Who really reads the fine print in full—especially when it’s hidden in another language or tucked away on the back of an official document? Probably not many. That’s why you should take a few minutes to read this article instead of combing through every detail on the back of your tax assessment. There’s one crucial piece of information that could cost you thousands of francs if overlooked. This article offers insights and takeaways from extensive experience in tax return preparation within our team.

What’s the difference between a tax assessment notice and the provisional tax bill? What is a final tax bill, and when is it due?

Check out our FAQ section and tax glossary for answers.

The fine print on the back

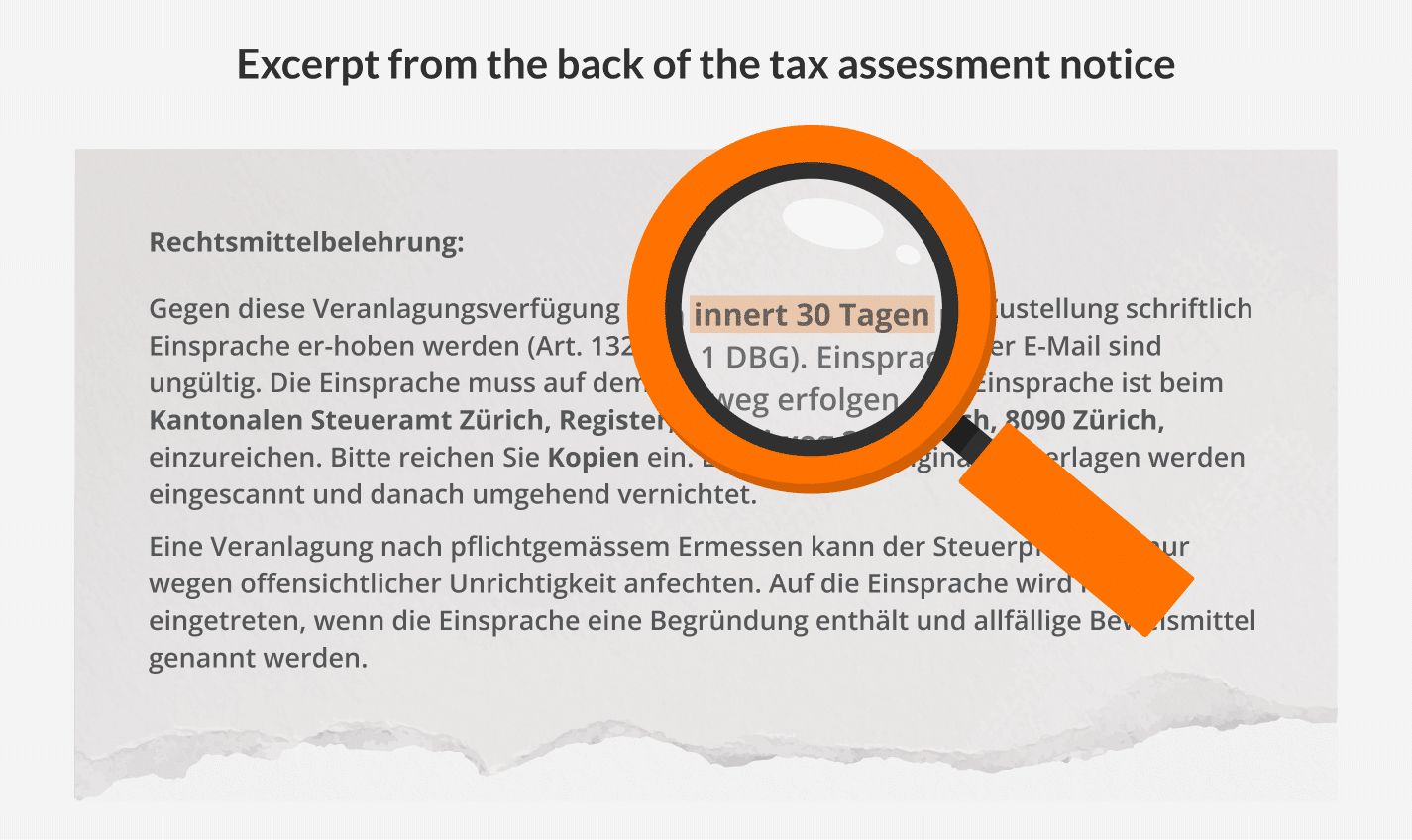

After submitting your tax return, you’ll eventually receive a tax assessment notice from the tax office—sometimes up to a year later. This notice summarizes your declared information and how it was processed by the tax authority. However, buried in the fine print on the back is a critical detail: you only have 30 days to file an objection.

Why is this 30-day objection deadline so crucial?

Even if your tax assessment contains obvious errors or results from a misunderstanding between you and the tax authority, this 30-day objection deadline still applies. Once those 30 days pass, it’s usually too late to make any corrections—no matter how valid your case is. People often overlook errors or notice them only much later—when it’s already too late.

Extensions are granted only in exceptional cases, such as prolonged hospital stays or time spent abroad. However, the bar is set high. In the case of being abroad, for example, you must provide airtight proof—like hotel bills and flight receipts—to justify your absence.

Common sources of errors – for expats

- Double taxation situations

- International (or intercantonal) tax allocations

- Entrepreneurs with their own businesses

- Holders of illiquid foreign assets

- Non-traditional family structures

- Discrepancies in net worth

Common issues include double taxation and errors in tax allocation, particularly when foreign income or assets are involved. These challenges are especially relevant for foreigners living in Switzerland, as foreign documents are often in other languages and tax systems can vary significantly. The complexity increases further when illiquid assets (such as real estate), highly volatile investments, significant equity interests (qualifizierte Beteiligungen), partial-year residency, or employee stock plans are part of the financial picture.

Example:

An expat living in Switzerland with a B permit and earning over CHF 120,000 owns shares in a foreign company and receives dividend payments and income from that company. Both are taxed at the source abroad. In Switzerland, however, he must declare them again (relevant for tax rate determination). A misunderstanding can easily lead to double taxation. If the 30-day deadline is missed, this becomes permanent—with no further opportunity to appeal.

How can a tax advisor help?

When people ask me what the main benefit of hiring a tax professional is, my answer is simple: the 30-day objection period. Sure, a tax advisor can help reduce your tax burden through skillful declarations and deductions—potentially saving you hundreds or even thousands of francs. But the real financial risk usually doesn’t lie in missed deductions. It lies in missing the objection deadline. That’s where the truly costly mistakes can happen.

Many people are busy and tend to set the tax assessment aside with the intention of reviewing it later—until it’s too late. Even if you spot the error yourself, it’s often nearly difficult or very expensive to find and brief a competent tax advisor and draft a solid objection within such a tight timeframe. If you had a tax advisor help prepare your return, you already have a point of contact who knows your situation.

While major mistakes are rare, the problem is you won’t know in advance when—or if—they’ll happen. A tax advisor can’t eliminate the risk completely, but their experience allows them to spot and evaluate red flags more effectively.

mit praktischen Tipps

und Beispielen für Ihre

private Steuererklärung

Zum Gratis Download

Leave Comment